Guest Post – Due Diligence: A Core Concept Underpinning the CSRD Framework

By: Reinhilde Weidacher, Managing Director, Head of EMEA Solutions, ISS Corporate Solutions

The European Sustainability Reporting Standards (ESRS), adopted at the end of July, require companies to comprehensively report on their due diligence processes under the four pillars of governance; strategy; impact, risk and opportunities; metrics and targets. This covers how companies embed due diligence in governance, strategy and business models, engage with affected stakeholders, identify and assess negative impacts on people and the environment, take action to address those impacts and track the effectiveness of these effort. At the same time, the ESRS don’t impose specific sustainability due diligence obligations.

Why Do Due Diligence Procedures Assume Such a Central Role?

- 3% of monitored companies[1] have faced grievances during the past 12 months over alleged negative human rights and environmental impacts at their operations or along their supply chains. A company’s ability to prevent such issues and, where that fails, respond to these grievances in a timely and relevant manner is paramount for sustainable economic development and is critical for the success of a business.

- Investors are paying close attention. Under the Sustainable Finance Disclosure Regulation (SFDR) they have to disclose a Statement on principal adverse impacts (PAIs) of investment decisions on sustainability factors. Mandatory indicators include the share of investments in companies that have been involved in violations of the UNGC principles or OECD Guidelines for Multinational Enterprises, as well as the share of investments in companies without policies to monitor compliance with those standards and/or mechanisms to handle grievances or complaints regarding possible violations.

- The concept of sustainability due diligence sets out procedures aimed at preventing and mitigating adverse impacts of business activities. It has been developed and refined through extensive stakeholder consultations since the early 2000s. The United Nations Guiding Principles on Business and Human Rights are a set of 31 principles organized under a 3-pillar framework: protect, respect and remedy. They were adopted by the UN Human Rights Council in 2011 and have since been widely endorsed by governments, NGOs and business. The OECD Guidelines for Multinational Enterprises are recommendations for responsible business conduct adhered to by 51 governments.

What is the Status of Endorsement of these Frameworks?

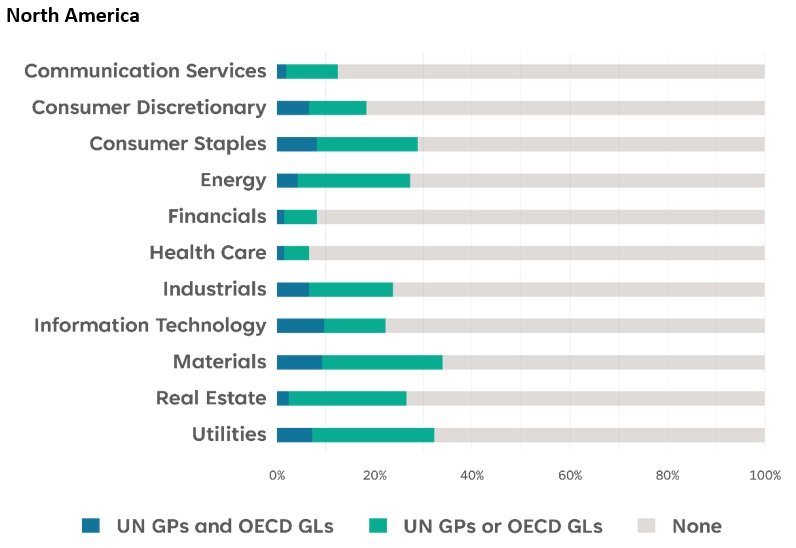

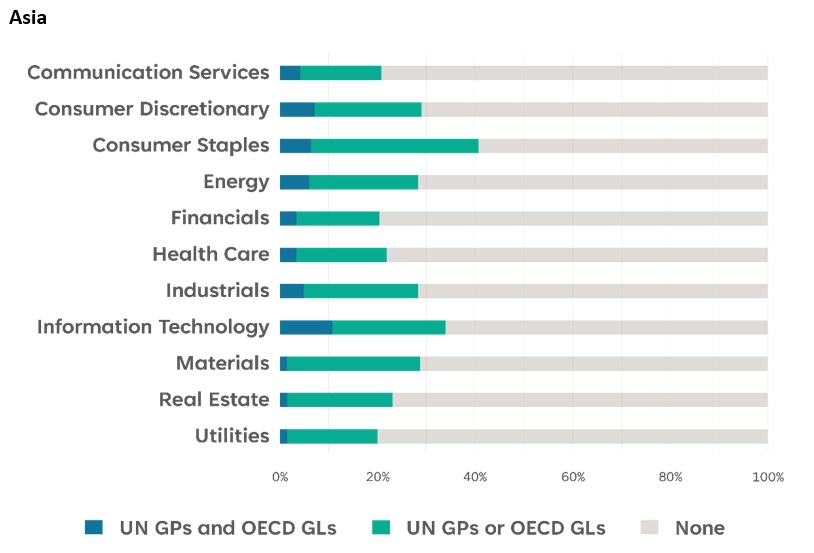

Endorsement of these frameworks varies widely between regions and industries, with Europe showing the highest level of support for the UN Guiding Principles on Business and Human Rights (UN GPs) and the OECD Guidelines for Multinational Enterprises (OECD GLs).

covering 8,800 companies globally, August 14, 2023

[1] ISS Corporate Solutions, ESG News Data, covering 17,250 companies globally, August 14, 2023.